By Dr John Wriglesworth, Executive Chairman at HERA Communications

Some may say that “housing is for nesting not for investing” but I say “because housing is for nesting it will always be good for investing”!

It seems that almost every day some expert economist will predict house price falls. The reasons they cite include:

- the Covid-19 pandemic (used as an excuse for anything bad that happens nowadays!)

- the expected Stamp Duty reintroduction, which some see as a precursor to house prices collapsing immediately after

- the changes to the Government’s Help to Buy scheme, which will eventually be phased out entirely, and will result in first time buyers needing higher deposits due to lenders consequently lowering their maximum Loan to Value ratios

- I have not even mentioned the threat of a recession this year!

Underpinning all of these factors, often used to predict doom and gloom on the house price front, is one key argument: the present high level of house prices is simply becoming unaffordable for too many prospective purchasers, especially first time buyers. Concluding that, if buyers cannot afford to buy, sellers will have to lower prices in order to sell.

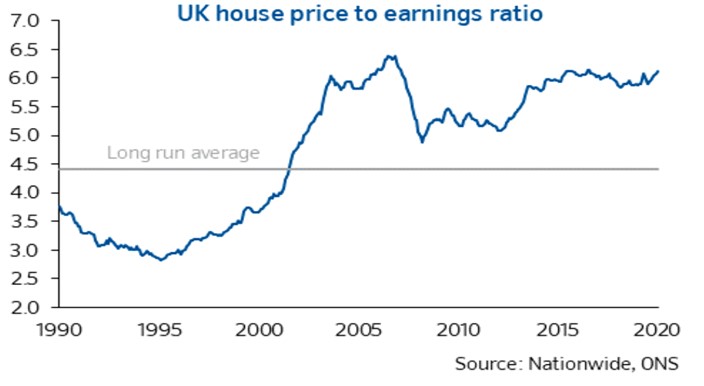

This argument is often backed up by referring to the “ratio of average house prices to average income”. This is presently over 6 times income and very high by historic standards see graph below.

It would seem obvious that buying a house which is valued at 6 times your annual income is totally unaffordable, and also compounding this argument is that no lender will lend more than 4 times income, which implies new buyers are typically requiring a cash deposit of twice their annual income.

However, in spite of this logic, over the past year house prices have risen by more than 6% according to many indices including the Nationwide House Price Index used in the above graph.

So why do house prices continue to rise?

While house prices are high relative to incomes, the cost of borrowing is very low. A typical new mortgage interest rate is presently 2.5%. Back in 1990 when the house price income ratio was around 3.5, mortgage interest rates were averaging a staggering 15%!

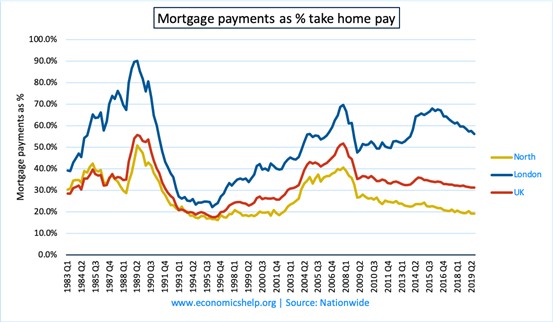

It does not take a genius to work out that a borrower paying 2.5% interest now can afford a much higher valued mortgage, and hence a higher priced home than if the interest rates were still 15%. The graph below shows the ratio of average mortgage repayments to earnings – currently the UK ratio is very close to the long time average (around 30%) and this suggests homeowners are not stretching themselves in paying off their mortgages. The average mortgage is now £140,000 where as in 1990 it was less than £35,000. But the cost of paying off the mortgage, relative to average income, is presently lower than in 1990.

It should therefore come as no surprise that house prices have been able to rise over the past 30 years!

What about deposits? Where is the magic money tree?

The above does not explain how new buyers can afford the very high cash deposits that are necessary, even with the availability of 95% LTV mortgages. The average house price in the UK is around £250,000 so a deposit will need to be at least £12,500. In London deposits for first time buyers typically need to be more than £50,000! Cue the magic money tree!

In all seriousness, there are two reasons why house purchases are still happening and, for many, are still affordable. First, most first time buyers are getting help from the “Bank of Mum and Dad”. Given the huge increase in house prices over the last 30 years, many middle aged households are sitting on a substantial amount of household wealth. Parents can easily extend their own mortgages and help their children out.

Secondly, we must remember those who cannot afford to buy are now typically tenants paying rent to a landlord. The private rental sector (PRS) has risen significantly over the last 20 years due to investor landlords buying up many properties to meet the huge increase in demand for rental accommodation from those who cannot afford to buy. These purchases have significantly helped sustain demand in the housing market filling the gap left by the reduction in first time buyers.

When the Stamp Duty (SDLT) holiday ends for homes under £500,000, will there be a fall in house prices?

If SDLT is reintroduced, buyers of an average priced home (around £250,000) will have to pay an extra 1% on their purchase. While there will be a rush to buy before the deadline and a lull afterwards, we need to remember that in the scheme of things a 1% increase in costs is not really significant. Over the last 12 months house prices have been rising by over 1% every two months and this has not caused house prices to fall. For a home purchased for £500,000 stamp duty will be 3%, more significant, but still not a crippling tax in the contest of the overall cost involved in buying.

We need to remember that house prices were still rising before the SDLT holiday which suggests house purchase demand will remain resilient after the short term lull following the pre rush to buy before it ends.

It is important to remember that we are an overcrowded island, with a growing population (despite Covid). People are living longer. Young people are leaving home earlier and divorce rates are high, resulting in one household turning into two! Demand for housing will continue to rise, as every one of us needs a roof over our head.

The only way the current market conditions will not result in future higher house prices, is if the supply of homes significantly increases. Despite many ambitious Government plans and targets, this simply has not happened and is not likely to happen to any significant degree in the near future.

So as a result house prices will continue to rise for the foreseeable future. As I said at the beginning “because housing is for nesting it will always be good for investing”!